With declining oil prices since mid-2014, the Subsea sector has seen a sharp fall in tree orders, with Infield Systems seeing a 29% reduction in demand between the second and third quarters of 2014. With this dramatic shift in the short-term global outlook, Infield Systems brings to the market its 2015 Subsea Market Report to 2019; examining the global market over the forthcoming five years and shedding light on how the subsea market is likely to be affected by the recent changes in oil prices and continued volatility within the market. Indeed, low oil prices have prompted E&P companies to re-evaluate their strategies, particularly regarding those deep and ultra-deepwater projects with high associated risks. Due to the nature of such developments the subsea sector has, and is likely to continue to see, considerable exposure to the volatility of the market.

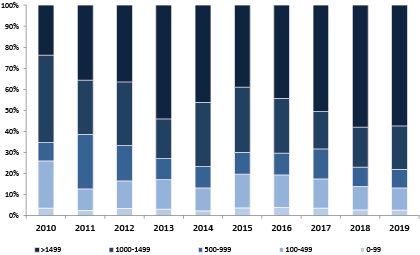

Despite this uncertainty, which may continue into 2016, Infield Systems remains positive for the growth of the subsea sector over the longer period to 2019. Currently, Infield Systems forecasts subsea tree orders to be up some 16% over the 2015-2019 timeframe compared with the previous five year period, with a potential Capex CAGR growth of over 11% across the entire subsea sector. The deepwater giants of Brazil, the Gulf of Mexico (GoM) and West Africa are expected to continue to drive demand over the longer term, with Infield Systems expecting the ultra-deepwater market (=>1,500m) to rebound from 2016 onwards. Indeed, global ultra-deepwater expenditure is forecast to account for 51% of demand over the entire five year period to 2019. At the same time, Infield Systems expects Asia and Australasia to see significant demand increases over the forecast timeframe, with these two regions not expected to be affected by the drop in subsea tree orders seen elsewhere in 2014. From an operator perspective, Petrobras is expected to ride out its present difficulties and continue to drive the market, with the NOC projected to account for a potential 25% share of global subsea Capex demand and a 16% share of subsea tree installations over the 2015-2019 timeframe. French giant Total is also expected to remain a strong driver of subsea investment demand, whilst Shell and BP are anticipated to remain key players within the GoM and West Africa markets.

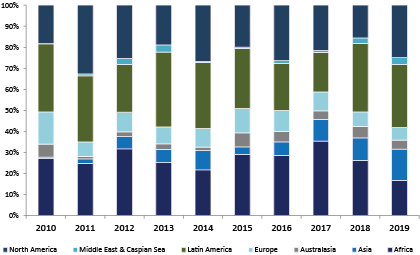

Global Subsea Capex (%) by Region 2010-2019

Global Subsea Capex (%) by Water Depth (m) 2010-2019

Looking specifically at the regional markets, Infield Systems expects the largest proportion of global subsea Capex over the forthcoming five years to be held by Africa at a 27% share, led by demand from Angola, Nigeria and Ghana. The majority of subsea investment in West Africa is expected to be directed towards developments at water depths of 1,000m and greater, with a peak year of spend projected for 2017. Offshore West Africa, Angola is expected to lead subsea investment demand, with a 58% share of regional demand. Here, key fields are anticipated to include Total’s Kaombo 1 and 2 developments, whilst expansion of BP’s Plutonio and PSVM projects is forecast to continue to demand significant spend. Nigeria’s offshore investment potential is likely to continue to remain uncertain, not least as a result of the floundering Petroleum Industry Bill (PIB), which has thus far taken five years to bring to a vote. However, over the medium term Infield Systems expects Subsea investment within the country to remain strong, driven by Total’s Egina field. Within the East African market, a key area of growth over the forthcoming five year period, Infield Systems anticipates subsea activity to continue to focus upon projects within the Rovuma Basin offshore Mozambique. In terms of spend, Anadarko is expected to lead the operators looking to gain from this frontier region, with the Prosperidade field driving the operator’s investment demand. The consortium of Eni and CNPC is also expected to invest substantially offshore Mozambique going towards 2019, with the Coral field expected to demand the highest subsea expenditure, particularly within the final year of the forecast.

The Latin American market will continue to be dominated by Brazil’s large deepwater developments if Petrobras can push ahead with most of its ambitious US$220.6billion 2014-2018 investment plan. Whilst the ultra-deepwater market is expected to be the hardest hit by 2014’s oil price decline, activity offshore Brazil, particularly within the ultra-deepwater market, is anticipated to ramp-up significantly beyond 2017. Indeed, Infield Systems’ Subsea Market Report to 2019 highlights a projected 89% subsea capital expenditure increase across the Latin America region between the years 2017 and 2018, predominantly as a result of the increasing levels of investment needed in a number of projects offshore Brazil, which include Petrobras’ Sururu, Berbiago and the Lula Alto fields. In time, and with increasing stability within the market, deepwater Mexico is also anticipated to attract increasing operator interest. As a result, the subsea sector is expected to witness further increases in demand offshore Latin America.

Offshore North America, projects within the GoM will continue to drive demand. In terms of subsea expenditure, Infield Systems expects 2015 to see a -48% decline on the previous year. However, from 2016 the market is expected to pick up, with 2019 seeing subsea investment levels second only to Latin America. Over the five year period most notable projects are anticipated to include Shell’s Stones development - with peak subsea spend in 2016 - ExxonMobil’s Hadrian North and Anadarko’s Heidelberg developments. In operator investment terms, Shell is expected to hold a leading 21% Capex share over the 2015-2019 timeframe, followed by BP (11%) and Anadarko (10%).

Offshore Asia, although not entirely unaffected by the recent decline in oil prices, Infield Systems expects for year on year growth throughout the forecast timeframe with a subsea Capex CAGR of 62% between 2015 and 2019. Expenditure is expected to continue to be driven by the South East Asian sub-region, in particular developments associated with the Gumusut-Kakap hub, Senangin and Ubah offshore Malaysia. Subsea demand is also expected to see growth offshore Indonesia and Brunei amongst others during the longer term to 2019. Elsewhere in the region, Infield Systems also expects strong growth offshore India, predominantly as a result of demand from the ONGC operated Krishna-Godavari fields and the Reliance-operated Dhirubhai D6-R series fields. Indeed, India’s need to fuel its growing economy has pushed operators to explore in deepwater environments, which will ultimately have a positive effect on the region’s subsea market.

Within the European region Infield Systems forecasts the highest number of potential subsea satellite projects to be installed globally over the 2015-2019 timeframe. Norway and the UK are anticipated to hold a combined 94% share of installations, whilst in subsea Capex terms Norway is expected to hold a 49% share, followed by the UK (44%). Other countries within the region that are expected to see subsea demand include: Italy, Ireland and Denmark amongst others. Key field developments are expected to include Eni’s Goliat, which is forecast to form a 28% share of Europe’s subsea capital expenditure demand during 2015 and the continued development of Ormen Lange, whilst the Quad 204 Schiehallion redevelopment over the medium-term to 2018 and Johan Sverdrup towards the end of the five year forecast period to 2019 are also likely to witness subsea expenditure.

Offshore Australasia, Australia is expected to see continued growth throughout the forecast timeframe, with subsea Capex associated with Chevron, Woodside and partners projects driving demand. Just under 80% of Chevron’s operated fields subsea Capex is expected to relate to developments within the Greater Gorgon Area. Subsea tree installation is expected to increase across the region with fields anticipated to see the largest number of installations likely to include Inpex’s Ichthys and Shell’s Prelude fields. The majority of subsea Capex offshore Australia is forecast to be directed towards projects situated in water depths of between 100 and 499 metres.

Looking towards the Middle East and Caspian Sea region, Infield Systems has forecast substantial subsea demand growth from 2018 onwards. Israel and Azerbaijan were expected to drive this, with Noble’s Leviathan field holding the potential to become the key project for subsea investment in the region. However, difficulties have emerged to delay this project significantly. In terms of tree installations, BP’s Shah Deniz (phase 2) development is likely to hold the largest share of demand, whilst other significant projects include Total’s Absheron project , and the continued development of Noble’s Tamar SW project offshore Israel.

Whilst the subsea investment market has been one of the hardest hit sectors as a result of oil price volatility, Infield Systems’ Subsea Market Report to 2019 highlights how this pivotal market within the offshore industry is anticipated to see the return of strong growth as a result of the resurgence of ultra-deepwater development forecast to take place beyond 2016. From an operator perspective, Petrobras, despite recent financial difficulties is expected to continue to be the key operator driving subsea investment, with Infield Systems’ forecast to 2019 seeing a US$19billion Capex requirement difference between the Brazilian NOC and its nearest global competitor.