Africa Oil Week: Stand 45

Infield Systems launches its new online Africa report; highlighting the

major trends and developments taking place across the region’s offshore sector.

Expected to hold a 20% share of global offshore Capex demand over the 2015-2019

timeframe, Africa, driven by deepwater development offshore Angola, Nigeria and

Ghana, remains a pivotal market for the world’s leading IOCs, with operators

including Total, Eni, BP, ExxonMobil and Independent Tullow all continuing to

invest a significant proportion of their E&P budgets within the region.

|

|

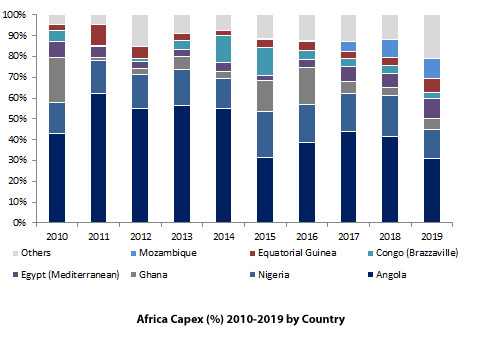

Infield Systems forecasts the Africa region to undergo a CAGR

of 14.5% in offshore Capex demand during the 2015-2019 timeframe. West Africa drives

this demand and is expected to hold an 80% share of African offshore Capex over

the five year period, although this represents a decrease from the previous

period to 2014 (91%), predominantly as a result of the growth projected for the

South and East African sub-region, driven by Mozambique. The North African

sub-region is also anticipated to see considerable Capex growth compared to the

historical period, primarily as a result of planned capital-intensive projects

such as the possible gas export pipeline from Israel’s Leviathan field to

Egypt.

Within West Africa, demand is

anticipated to remain driven by Angola with key projects including: Total’s

Kaombo 1 and 2 and the possible Chissonga development operated by Maersk. Altogether, Infield Systems expects a total

of 111 fields offshore Angola to require Capex spend, whilst average water

depths of developments are forecast to stand at around 900 metres. Nigeria is

expected to remain the second highest demand driver with forecast Capex

expected to increase by 107% compared to the previous five years; predominantly

as a result of the giant Egina project, which is expected to form 40% of

Nigeria’s offshore Capex over the period. Ghana is expected to comprise 8% of

Africa’s offshore Capex over the 2015-2019 timeframe, with the largest demand expected

to be required by the subsea sector; driven by projects such as Tweneboa (TEN)

and Mahogany East.

|

Within the South and East African

sub-region Infield Systems expects the consortium of Eni CNPC to lead development

spend, with activities solely focused upon projects offshore Mozambique, in

particular the Coral and Mamba North and South prospects. Anadarko is also

expected to direct investment towards developments offshore Mozambique,

focusing on prospects within the Prosperidade area. Investment offshore

Tanzania could also commence towards the end of the timeframe, whilst offshore

Namibia, the Kudu field, operated by NOC Namcor, remains on the table for

development before the end of the decade although further delays may also be likely here.