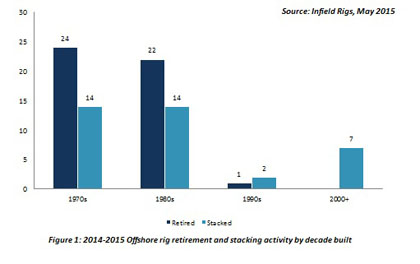

Since the current offshore drilling downturn began, the rig market has seen a swathe of retirements and units being cold stacked. Indeed, over the last eighteen months 38 floaters and 15 jackups have been retired from service whilst a total of 38 assets have been cold stacked. Whilst these numbers certainly seem high when compared to historical averages, at the current rate they are unlikely to trigger a recovery in charter rates and utilisation. In order for this to happen, the rate of retirements must outpace the rate at which newbuilds are delivered; otherwise both may continue to decline. As noted above the majority of retirement activity has taken place in the floating rig market, with 33 semi-subs and four drillships retired thus far. Retirement activity has picked up as rig managers look to stem the accelerated decrease in floating rig utilisation, which has fallen from 91% in April 2014 to 82% in May 2015.

|

As well as retirements, the market has seen a significant increase in the number of rigs being cold stacked. Cold stacking is attractive to rig managers as it means OPEX costs can be lowered and the unit can still be considered for reactivation if and when the market picks up. When considering to cold stack an asset, the rig owner must balance the combined costs of deactivation/re-activation against the cost of continuing to actively market the asset. During the cold stacking decision making process a rule of thumb that is often applied by rig managers relates to the expected duration of inactivity. Indeed, if the unit is not expected to win a contract for a minimum period of two years, cold stacking becomes a viable option. The majority of stacking activity in the current cycle has been focused on older jackup rigs and rather than being stacked, these units need to be retired from the global fleet. The average age of jackups cold stacked during the 2H 2014/2015 period stands at 35 years, making it highly unlikely that these units will be reactivated. By permanently removing these older units from the fleet,managers could create greater opportunities for the large supply of newbuild rigs set to enter the market.

|

The current rise in retirement andstacking activity is a positive for the industry. However, whilst such anoversupplied market exists, greater retirement activity for less capable andageing assets is required. Infield Systems believes that the market is yet towitness a large enough rise in jackup retirements and believes that currentactivity needs to go further if the market is to rebalance in the future.

Delivery delays

begin to pick up/are cancellations likely?

In an attempt to offset the currently

oversupplied market, a number of rig managers have proactively agreed to

delivery delays for some of their newbuild assets. By delaying delivery,

managers will limit the impact of lower charter rates and utilisation whilst

also pushing newbuild payment schedules to the right. Some of the agreed upon

delays are listed below:

|

Rig Name

|

Rig Manager

|

Rig Type

|

Country of Build

|

Group Yard Name

|

Original Delivery Quarter

|

Length of Delay

|

Comments

|

|

Jap Driller 1

|

Jap Drilling Ltd

|

Jackup

|

China (PRC)

|

ZPMC

|

Q1 2015

|

Not Specified

|

Delivery has been delayed due to market downturn

|

|

Ocean Rig Crete

|

Ocean Rig

|

Drillship

|

South Korea

|

SHI

|

Q1 2017

|

12 Months

|

Deferred portion of pre-delivery costs, reducing Capex obligation

|

|

Ocean Rig Amorgos

|

Ocean Rig

|

Drillship

|

South Korea

|

SHI

|

Q2 2017

|

18 Months

|

Deferred portion of pre-delivery costs, reducing Capex obligation

|

|

Transocean Cepheus

|

Transocean

|

Jackup

|

Singapore

|

Keppel

|

Q1 2016

|

24 Months

|

Transocean has delayed delivery of the unit twice

|

|

Transocean Cassiopeia

|

Transocean

|

Jackup

|

Singapore

|

Keppel

|

Q2 2016

|

27 Months

|

Transocean has delayed delivery of the unit twice

|

|

Transocean Centaurus

|

Transocean

|

Jackup

|

Singapore

|

Keppel

|

Q3 2016

|

30 Months

|

Transocean has delayed delivery of the unit twice

|

|

Transocean Cetus

|

Transocean

|

Jackup

|

Singapore

|

Keppel

|

Q1 2017

|

30 Months

|

Transocean has delayed delivery of the unit twice

|

|

Transocean Cirinus

|

Transocean

|

Jackup

|

Singapore

|

Keppel

|

Q2 2017

|

33 Months

|

Transocean has delayed delivery of the unit twice

|

|

Atwood Admiral

|

Atwood Oceanics

|

Drillship

|

South Korea

|

DSME

|

Q1 2015

|

12 Months

|

Delay can be extended to September 2016

|

|

Atwood Archer

|

Atwood Oceanics

|

Drillship

|

South Korea

|

DSME

|

Q4 2015

|

Six Months

|

Delay can be extended to June 2017

|

|

Energy Engager

|

Northern Offshore

|

Jackup

|

China (PRC)

|

COSCO

|

Q1 2016

|

Nine Months

|

Delayed due to market downturn

|

|

Energy Encounter

|

Northern Offshore

|

Jackup

|

China (PRC)

|

COSCO

|

Q3 2016

|

Nine Months

|

Delayed due to market downturn

|

|

Fecon Jackup TBN 1

|

Fecon

|

Jackup

|

Singapore

|

Keppel

|

Q3 2016

|

Six Months

|

Delayed due to market downturn

|

|

Fecon Jackup TBN 2

|

Fecon

|

Jackup

|

Singapore

|

Keppel

|

Q3 2016

|

Six Months

|

Delayed due to market downturn

|

|

Fecon Jackup TBN 3

|

Fecon

|

Jackup

|

Singapore

|

Keppel

|

Q4 2016

|

Six Months

|

Delayed due to market downturn

|

|

Stena MidMax II

|

Stena Drilling

|

Semisub

|

South Korea

|

SHI

|

Q4 2016

|

-

|

Stena extended the option to cancel the unit until Spring 2015

|

Table 1: Announced newbuild rig

delays in 2015

Source: Infield Rigs (May 2015)

Whilst delaying deliveries is clearly an attractive strategic

option in the current climate, it does not make sense for every rig manager.

For instance, Pacific Drilling (“Pacific”)

is set to take delivery of the Pacific Zonda drillship in Q4 2015 and the

company has chosen not to delay its delivery. The reason behind this decision

is that Pacific has a strong construction contract which calls for liquidated

damages from the shipyard for late delivery. As such, it remains in the

company’s interest to maintain the delivery dates that the yard can provide

rather than delay delivery. Upon delivery Pacific plans to either stack the

unit at a shipyard in South Korea or if contracting levels have picked up,

mobilise the unit to the US GoM.

However, Pacific’s choice of action for the Pacific Zonda may

prove to be an exemption rather than the rule as other managers including

Atwood Oceanics and Ocean Rig have taken the decision to delay delivery of

newbuild drillships. Indeed, each delivery is likely to be reviewed on a case

by case basis by rig managers and is heavily dependent upon the agreed

construction contract and the prevailing market conditions at the time of

delivery.

By delaying deliveries, rig managers have the opportunity to

partially mitigate the current supply glut. In addition, charter rates for floating rigs

have witnessed a dramatic decline in 2015 and this is likely to further

discourage rig managers from taking delivery of newbuild assets. Whilst

cancellations have been discussed, especially in relation to speculative rig orders,

none have been reported, as yet.

From a regional perspective, the most at risk rig builders

can be found in China, where yards enticed speculative owners into placing

orders at attractive payment terms. Here it was not uncommon for owners to be

only required to pay a 5% down payment and in certain cases, as little as 1% or

2% (Jap Driller 1 jackup is a prime example). This is an advantage to

speculative owners who, in the event of being unable to secure a contract for

their asset, can walk away from their order with relatively little loss.