Having enjoyed a period of sustained growth the floating rig

market has cooled, significantly. New fixtures have evaporated and the few that

have been inked have been agreed at significantly lower rates. Competition for

tenders has been fierce as a greater number of managers have vied for fewer

contracts. To make matters worse, the current environment of demand erosion has

coincided with rapid supply-side growth, with utilisation being hit hard as a

consequence. With negative pressures persisting on both the supply and demand

sides, many market participants are wondering how far the market will fall and

when a rebound should be expected.

From boom to bust… again

The offshore industry has long been at the whim of the

global economy. On several occasions the market has seen periods of sustained

growth followed by acute contraction, the global financial crisis being a prime

example. Indeed, the global recession of 2008/09 ended a period of record

charter rates and rig counts as assets were laid up en masse amid a commodity

price collapse. Despite the severity of the downturn it was short-lived, and as

oil prices rallied so to do did investment in deepwater E&P with rig rates

and counts following suit. This positive post-recession environment encouraged

asset investment, with new players entering the market and incumbents renewing

and expanding their fleets.

The latest downturn has had a very different feel. Even

before the price of oil began to slide operators margins were being squeezed as

a stagnant (albeit high) oil price was met with increasing costs. Consequently,

less profitable projects were postponed and exploration budgets cut. The

situation deteriorated in the second half of 2014 as global oil demand failed

to keep pace with supply and the price of Brent tanked. As of July the oil

markets remain oversupplied and the outlook remains uncertain. Indeed, output

from OPEC, Russia, the US and Brazil continues apace and gains in Iran are

beginning to seem increasingly likely. Brent is unlikely to recover far beyond

the US$60 per barrel mark until excess supply is whittled away. Even when a

concerted recovery is established, any gains will likely be capped by US

onshore tight oil production, the new swing producer. It is hard to see Brent

rebounding anywhere near US$100 per barrel anytime soon.

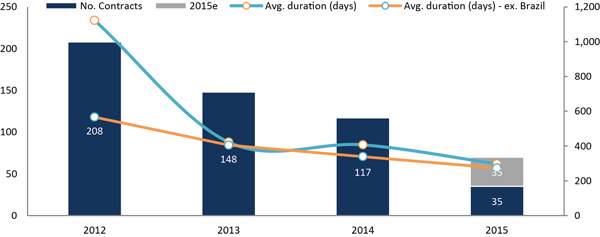

Figure 1: New fixtures for floating rigs (Source: InfieldRigs)

The turmoil of the past 12 months has had a profound effect

on the drilling markets. The number of floating rig fixtures has plummeted and

average contract durations have shortened, see Figure 1 above. Indeed, just 35

new contracts were signed in the first six months of 2015, many of which

related to short-term work or single well programmes. Whilst a handful of more

significant fixtures have been signed, a more telling trend has been the

renegotiation of current contracts, often for extended duration, as seen with

Oranje-Nassau Energie’s deal with Paragon for the C461 jackup. More worryingly the market has seen many

assets idled and a number of contract cancellations, illustrated by BP’s

termination of the West Sirius contract, thereby slashing some US$160 million

from Seadrill’s backlog. Other high-profile causalities have included the ENSCO

DS-9, ENSCO DS-4, Belford Dolphin, COLSLPioneer and Stena Carron. If low oil

prices persist the market may well see further examples of premature contract

cancellations.

Contract visibility

The recent scarcity of new fixtures has meant many rigs

rolling off contract have been idled. As a result utilisation rates have

plunged and drilling contractors have begun to retire their older less capable

rigs. Cold stacking has been a common theme also, and not just for ageing

assets. Indeed, ENSCO took the bold decision to stack the 8501 and 8502 semis in

order to reduce operating costs until market conditions improve.

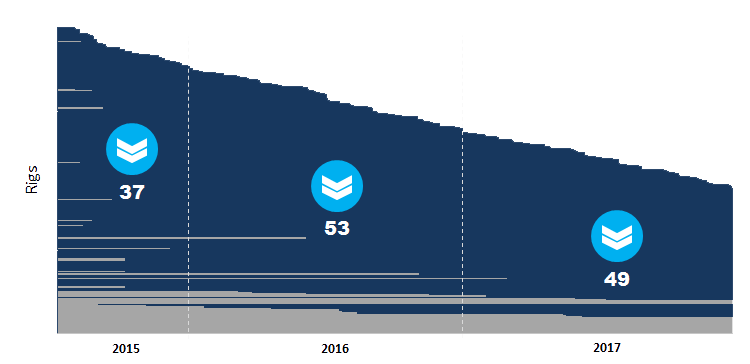

According to InfieldRigs data, 51 floating rigs are ready

stacked as of July, up from 17 this time last year. With few contracts being

signed and many nearing completion, the number of idled assets is expected to

increase through 2015 and 2016. Indeed, Figure 2 below shows visible contracted

demand (including options) for drillships and semisubs. Current visibility

indicates that a minimum of 37 additional floaters will roll off contract this

year (assuming all options are exercised), significantly adding to the idled

fleet. As a result utilisation will fall further and contractors will be

encouraged to remove their less competitive assets from the market.

Figure 2: Contract Gantt Chart(Source: InfieldRigs)

On a regional basis, the majority of the idle fleet is

currently situated in South East Asia, the Mediterranean, the US Gulf of Mexico

and West Africa. Looking ahead through the remainder of 2015, the North Sea,

North America, West Africa and Latin America are expected to see the lion’s

share of rigs rolling off contract.

Rig counts

The number of contracted floating rigs peaked at 275 in

September 2014 and has since been in relatively steep decline, with July’s

count standing at 230. The steepest declines have been witnessed in Brazil

(down from 63 in Sep-14 to 51 in Jul-15, though the market has fallen from 79

at the beginning of 2013), West Africa (down 10 from 39 in Oct-14) and South

East Asia (down 6 from 13 in Sep-14).

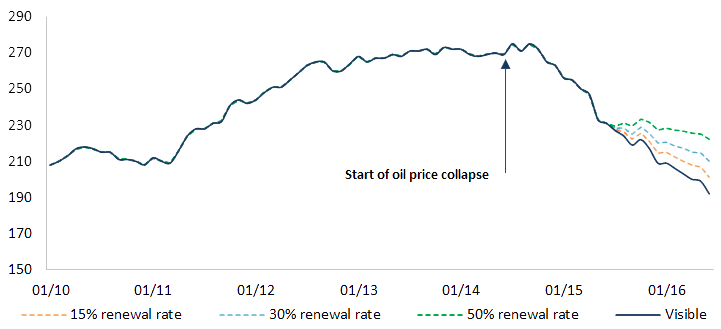

Figure 3 below shows the floating rig count trend from

January 2010 to present day, with three renewal-rate sensitivity scenarios for

the coming 12 month period. Current visibility (including new builds, 100%

exercised options and no renewals) shows the fleet count to continue to fall to

192 contracted drillships and semisubs by June 2016. The three alternative

views, based on the same assumptions as above but with contract renewal rate

set at 15%, 30% and 50% respectively shows the fleet to fall to 201, 210 and

223 respectively by mid-2016.

Figure 3: Rig counts with renewal rate sensitivity(Source: InfieldRigs)

Whilst the above assumptions are simplistic in nature, they

are grounded in real data and illustrate the likely trend over the next 12

months. However, in reality we may see far fewer options being exercised and a

higher rate of renewals, with significant variation from region to region.

Moreover, as the current downturn persists the market may witness further

contract cancellations, putting further downward momentum on counts. One

certainty is that the rig count nadir always lags the oil market downturn, so

further declines should be expected so long as Brent remains below US$60 per

barrel.

Where next?

The floating rig market has fallen hard and current evidence

is indicative of harder times to come over the next 12 to 18 months, and

possibly longer. Consensus suggests that Brent will average around US$65 per

barrel in 2016, not high enough to encourage any significant volume of

contracting activity or E&P budget increases. The market is therefore

likely to remain supressed through 2016, with a tentative recovery expected

sometime in 2017. Indeed, given the long-term nature of this latest downturn

the market is unlikely to see rig counts reach their previous highs until 2019

at the earliest.